Click image

for larger version

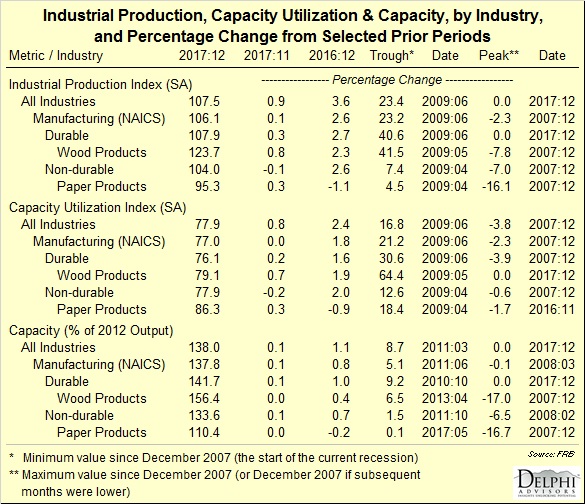

Total

industrial

production (IP) rose 0.9% in December (+0.4% expected)

despite manufacturing output edging up by only 0.1% (+0.3% expected). Revisions

to mining and utilities altered the pattern of growth for October and November,

but the level of the overall index in November was little changed. For 4Q as a

whole, total IP jumped 8.2% at an annual rate after being held down in 3Q by

Hurricanes Harvey and Irma. At 107.5% of its 2012 average, the index has

increased 3.6% since December 2016 for its largest calendar-year gain since

2010. The gain in manufacturing output in December was its fourth consecutive

monthly increase. The output of utilities advanced 5.6% for the month, while

the index for mining moved up 1.6%.

Click image

for larger version

Click image

for larger version

Industry Groups

In

December, manufacturing output edged up 0.1% and was 2.4% above its

year-earlier level. In 4Q, the index for manufacturing moved up at an annual

rate of 7.0%. The gain in manufacturing in December reflected increases of 0.3%

and 0.2% in the indexes for durables and for other manufacturing (publishing

and logging), respectively; the index for nondurables edged down 0.1%. Within

durables, gains were widespread, with the largest advance, 2.0%, registered by

motor vehicles and parts (wood products:

+0.8%). Among nondurables, increases for most major industries were offset

by declines in petroleum and coal products, in chemicals, and in plastics and

rubber products (paper products: +0.3%).

The

output of mines rose 1.6% in December primarily because of a gain posted by oil

and gas extraction; the index was up 11.5% from its year-earlier level. In 4Q, mining output advanced at an annual rate of 12.7% after being

held down by the hurricanes in 3Q.

Click image

for larger version

Capacity

utilization (CU) for the industrial sector was 77.9%, a rate that is 2.0

percentage points below its long-run (1972–2016) average.

Capacity

utilization in manufacturing was unchanged at 76.4% in December and remained

2.0 percentage points below its long-run average. Utilization for durables

edged up 0.1 percentage point to 76.1%, and the operating rate for nondurables

edged down 0.1 percentage point to 77.9% (wood

products: +0.7%; paper products: +0.3%).

The operating rate for mines rose 1.2 percentage points to 85.6%, and the rate

for utilities jumped 4.2 percentage points to 80.4%.

Click image

for larger version

Capacity

at the all-industries level nudged up 0.1% (+1.1% YoY) to 138.0% of 2012

output. Manufacturing (NAICS basis) rose fractionally (+0.1% MoM; +0.8% YoY) to

137.8%. Wood products: +0.0% (+0.4%

YoY) to 156.4%; paper products: 0.0%

(-0.2% YoY) to 110.4%.

The foregoing comments represent the

general economic views and analysis of Delphi Advisors, and are provided solely

for the purpose of information, instruction and discourse. They do not

constitute a solicitation or recommendation regarding any investment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.