Click image

for larger view

Click image

for larger view

Sales

of new single-family houses in November 2016 were at a seasonally adjusted

annual rate (SAAR) of 592,000 units (580,000 expected).

That was 5.2 percent (±14.1%)* above the revised October rate of 563,000 and 16.5

percent (±19.3%)* above the November 2015 estimate of 508,000 units; the

not-seasonally adjusted year-over-year comparison (shown in the table above)

was +13.9%. For a longer-term perspective, November sales were 57.4% below the “bubble”

peak and 21.6% below the long-term, pre-2000 average.

The

median sales price of new houses sold in November rose to $305,400 (+$2,700 or

0.9%); the average sales price increased by $5,200 (1.5%) to $359,900. Starter

homes (those priced below $200,000) comprised 14.6% of the total sold, up from

November 2015’s record-low 11.1% for that calendar month (going back to 2002);

prior to the Great Recession starter homes represented as much as 61% of total

sales. Homes priced below $150,000 made up 2.4% of those sold in November, a

further slide from November 2015’s previous record-low share of 2.8%.

* 90% confidence interval includes zero.

The Census Bureau does not have sufficient statistical evidence to conclude

that the actual change is different from zero.

Click image

for larger view

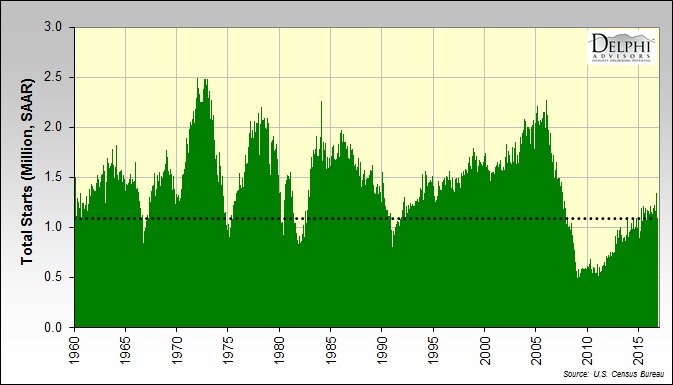

As

mentioned in our post

about housing permits, starts and completions in November, single-unit

completions rose by 25,000 units (+3.3%). Because completions and sales were

nearly balanced, new-home inventory expanded in absolute terms (+4,000 units) but

shrank in months of inventory terms (-0.1 month).

Click image for

larger view

Existing home sales

increased by 40,000 units (+0.7%) in November, to 5.61 million units (SAAR), well

above expectations

of 5.35 million. Inventory of existing homes shrank in both absolute (-160,000

units) and months-of-inventory (-0.3 month) terms. Although existing-home sales

outpaced those of new homes in November, the share of total sales comprised of

new homes expanded to 9.5%. The median price of previously owned homes sold in November

edged up by $800 (0.3%), to $234,900.

Click image

for larger view

Housing

affordability marginally improved as the median price of existing homes for

sale in October fell by $3,200 (-1.4%; but +5.9 YoY), to $233,700. Concurrently,

Standard & Poor’s

reported that the U.S. National Index in the S&P Case-Shiller CoreLogic Home

Price indices posted a not-seasonally adjusted monthly change of +0.2% (+5.6% YoY),

bringing home prices to a new all-time high.

“Home

prices and the economy are both enjoying robust numbers,” said David

Blitzer, Managing Director & Chairman of the Index Committee at S&P

Dow Jones Indices. “However, mortgage interest rates rose in November and are

expected to rise further as home prices continue to outpace gains in wages and

personal income. Affordability measures based on median incomes, home prices

and mortgage rates show declines of 20-30% since home prices bottomed in 2012.

With the current high consumer confidence numbers and low unemployment rate,

affordability trends do not suggest an immediate reversal in home price trends.

Nevertheless, home prices cannot rise faster than incomes and inflation indefinitely.”

“After

the S&P CoreLogic Case-Shiller National Index bottomed in February 2012,

its year-over-year growth accelerated to a peak rate of 10.9% in October 2013

and then gradually fell to its current rate of approximately 5%. During the

same period, the highest year-over-year rate from any city was 29% in August

and September 2013; currently the highest single city gain declined to

approximately 11%. Both national and city growth in home prices slowed but

remains above the growth rate of incomes and inflation.”

Click image

for larger view

The foregoing comments represent the

general economic views and analysis of Delphi

Advisors, and are provided solely for the purpose of information, instruction

and discourse. They do not constitute a solicitation or recommendation

regarding any investment.