Click image

for larger version

The

seasonally adjusted consumer price index for all urban consumers (CPI-U) increased

0.1% (as

expected)

in February -- the smallest MoM rise since July 2016. The gasoline index

declined, partially offsetting increases in several indexes, including food,

shelter, and recreation. The energy index fell 1.0%, with the decline in

gasoline outweighing increases in the other energy component indexes. The food

index increased 0.2% over the month, its largest rise since September 2015.

The

index for all items less food and energy rose 0.2% in February. The indexes for

shelter, recreation, apparel, airline fares, motor vehicle insurance,

education, and medical care were among those that increased in February.

Indexes that declined include communication, used cars and trucks, new

vehicles, and household furnishings and operations.

The

all-items index rose 2.7% for the 12 months ending February; the 12-month

increase has been trending upward since a July 2016 trough of 0.8%. The index

for all items less food and energy rose 2.2% over the last 12 months; this was

the fifteenth straight month the 12-month change remained in the range of 2.1

to 2.3%. The energy index rose 15.2% over the last year, while the food index

was unchanged. Rent rose by 3.9% YoY, and medical services: +3.4%.

The

seasonally adjusted producer price index for final demand (PPI) increased 0.3%

(+0.1%

expected)

in February. Final demand prices rose 0.6% in January and 0.2% in December. Over

80% of the advance in the final demand index is attributable to a 0.4% increase

in prices for final demand services; final demand goods moved up 0.3%.

Prices

for final demand less foods, energy, and trade services rose 0.3% in February,

the largest increase since a 0.3% advance in April 2016. For the 12 months

ended in February, the index for final demand less foods, energy, and trade

services climbed 1.8%.

The

final demand index climbed 2.2% for the 12 months ended February 2017, the

largest YoY advance since a 2.4% increase in March 2012.

Final Demand

Final

demand services: The index for final demand services moved up 0.4% in February,

the largest advance since a 0.4% increase in June 2016. Nearly 70% of the

February rise can be traced to prices for final demand services less trade,

transportation, and warehousing, which climbed 0.5%. The indexes for final

demand trade services and for final demand transportation and warehousing

services advanced 0.4% and 0.3%, respectively.

Product

detail: In February, a major factor in the increase in prices for final demand

services was the index for traveler accommodation services, which rose 4.3%.

The indexes for chemicals and allied products wholesaling; legal services;

apparel wholesaling; health, beauty, and optical goods retailing; and

architectural and engineering services also moved higher. In contrast, the

index for automotive fuels and lubricants retailing fell 10.0%. Prices for

wireless telecommunication services and for securities brokerage, dealing, and

investment advice also decreased.

Final

demand goods: Prices for final demand goods moved up 0.3% in February, the

sixth consecutive rise. Over half of the broad-based February increase can be

traced to the index for final demand energy, which advanced 0.6%. Prices for

final demand foods and for final demand goods less foods and energy moved up

0.3% and 0.1%, respectively.

Product

detail: Nearly 70% of the February increase in prices for final demand goods is

attributable to the index for electric power, which climbed 1.6%. Prices for

fresh and dry vegetables, jet fuel, liquefied petroleum gas, pharmaceutical

preparations, and residual fuels also rose. Conversely, the index for gasoline

fell 2.5%. Prices for beef and veal and for search, detection, navigation, and

guidance systems and equipment also decreased.

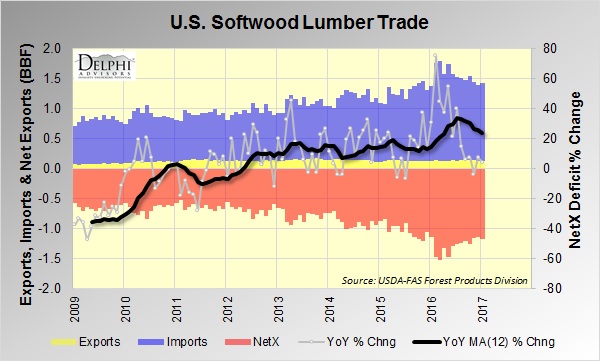

Click image

for larger version

Virtually

all of the not-seasonally adjusted price indexes we track rose on a MoM basis, and

all moved higher on a YoY basis.

Click image

for larger version

The foregoing comments represent the

general economic views and analysis of Delphi

Advisors, and are provided solely for the purpose of information, instruction

and discourse. They do not constitute a solicitation or recommendation

regarding any investment.