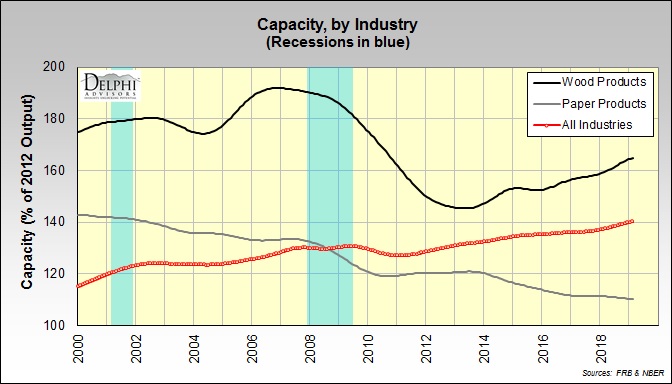

Click image

for larger view

Click image

for larger view

Softwood

lumber exports turned up (29 MMBF or +31.30%) to start the year in January; meanwhile,

imports fell (67 MMBF or -6.0%). Exports were 11 MMBF (-8.5%) below year-earlier

levels; imports were 99 MMBF (-8.6%) lower. As a result, the year-over-year

(YoY) net export deficit was 87 MMBF (-8.6%) smaller. Also, the average net

export deficit for the 12 months ending January 2019 was 2.9% smaller than the

average of the same months a year earlier (the “YoY MA(12) % Chng” series shown

in the graph above).

Click image

for larger view

North

America (44.7%; of which Canada: 19.6%; Mexico: 25.0%) and Asia (28.0%; especially

China: 9.5%) were the primary destinations for U.S. softwood lumber exports; the

Caribbean ranked third with a 20.5% share. Year-to-date (YTD) exports to China

were -63.3% relative to the same months in 2018. Meanwhile, Canada was the source

of most (87.2%) of softwood lumber imports into the United States. Imports from

Canada were 10.0% lower YTD than the same months in 2018. Overall, YTD exports

were down 8.5% compared to 2018; imports: -8.6%.

Click image

for larger view

Click image

for larger view

U.S.

softwood lumber export activity through the Gulf customs region represented the

largest proportion (33.3% of the U.S. total), followed by the West Coast (30.4%)

and Eastern (29.5%) regions. Seattle (18.8% of the U.S. total) maintained the lead

over Mobile (17.4%) as the single most-active district. At the same time, Great

Lakes customs region handled 59.0% of softwood lumber imports -- most notably the

Duluth, MN district (21.7%) -- coming into the United States.

Click image

for larger view

Click image

for larger view

Southern

yellow pine comprised 25.1% of all softwood lumber exports, Douglas-fir (11.6%)

and treated lumber (12.4%). Southern pine exports were down 32.3% YTD relative

to 2018, while treated: -20.2%; Doug-fir: -11.8%.

The foregoing comments represent the

general economic views and analysis of Delphi

Advisors, and are provided solely for the purpose of information, instruction

and discourse. They do not constitute a solicitation or recommendation

regarding any investment.