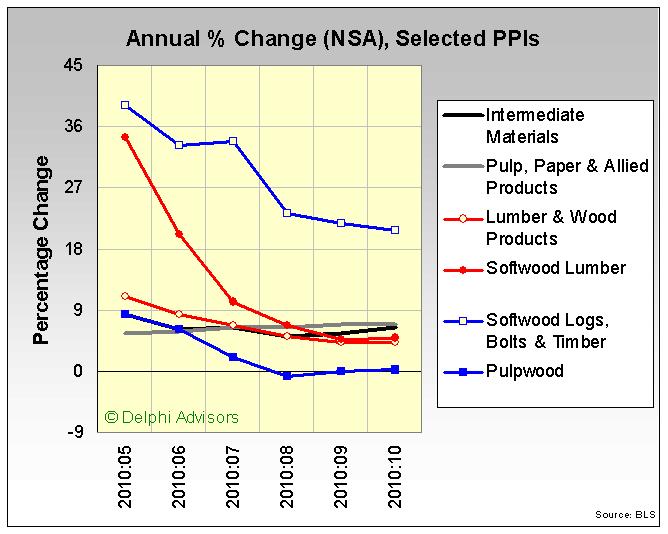

Click image for larger view

Click image for larger view

Overall

construction spending in the United States unexpectedly rose to $801.7 billion in September, led by increases in homebuilding and public projects. The 0.5 percent gain was made possible by a $14.4 billion downward revision to August’s estimates that turned a previously reported gain of 0.4 percent into a 0.2 percent drop.

Click image for larger view

Estimates of the changes in private residential spending and the number of total

housing starts agreed for once in September. Private residential spending rose 1.8 percent, while the number of total starts rose 0.3 percent to 610,000 -- a five-month high.. "At least we're making some progress here," said

John Herrmann, senior fixed income strategist at State Street Global Markets in Boston. "It's a slow, steady-as-she-goes improvement in builder activity."

Click image for larger view

Click image for larger view

All of the September gain in private residential starts was concentrated in the single-unit component (4.4 percent), as multi-family starts fell by 9.7 percent. On an annual-change basis, total starts were up 4.1 percent in September.

Click image for larger view

Despite a 6.6 percent jump in

new-home sales, substantially more houses were started than sold. The ratio of starts to sales hovered around 1.5 in September -- near the upper end of the “normal” historical range. On a more positive note, however, an uptick in completions did not prevent both the number of new homes for sale and months of inventory from declining.

Click image for larger view

Click image for larger view

Existing home sales jumped by an even greater amount (10.0 percent) than that for new homes, shrinking the inventory of existing homes and causing the proportion of total sales represented by new homes to drop to near 6 percent. The lowest mortgage rates on record and cheaper homes (the median resale price dropped 3.3 percent, to $171,700) appear to be luring some buyers off the sidelines.

Even with the jump in resales, however, “...[the market is] still at a remarkably depressed level,” said

Tom Porcelli, senior economist at RBC Capital Markets Corp. in New York. “We’re going to continue to muddle along here, given the supply- demand imbalance.”

Click image for larger view

The seasonally adjusted

S&P/Case-Shiller home price indices moved lower in every market except New York City between July and August.

Click image for larger view

“A disappointing report,” remarked David Blitzer, Chairman of the Index Committee at Standard & Poor’s. “Home prices broadly declined in August. Seventeen of the 20 cities and both Composites saw a weakening in [not-seasonally adjusted] year-over-year figures, as compared to July, indicating that the housing market continues to bounce along the recent lows. Over the last four months both the 10- and 20-City Composites show slowing growth, after sustaining consistent gains since their April 2009 troughs.

“The month-over-month growth rates tell the same story. Fifteen of the 20 metropolitan statistical areas and the two Composites saw a decline in the month of August as compared to July levels. The 10- and 20-City Composites fell 0.1 percent and 0.2 percent, respectively. Indeed, the housing market appears to have stabilized at new lows. At this time, it does not seem that any of the markets are hanging on to the temporary momentum caused by the homebuyers’ tax credits.”

Click image for larger view