Click image

for larger version

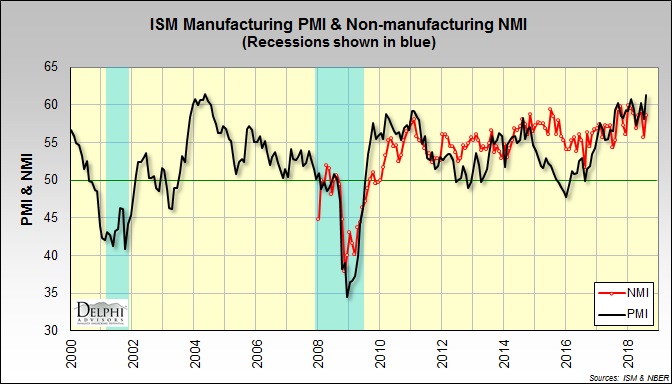

The Institute for

Supply Management’s (ISM) monthly sentiment survey showed that the

expansion in U.S. manufacturing accelerated in August. The PMI

registered 61.3%, down 3.2 percentage

points (PP) from the July reading.

(50% is the breakpoint between contraction

and expansion.) ISM’s

manufacturing survey represents under 10% of U.S. employment and about 20% of

the overall economy. “This indicates strong growth in

manufacturing for the 24th consecutive month, led by continued expansion in all

subindexes that make up the PMI,” said Timothy Fiore, Chair of ISM’s Manufacturing

Business Survey Committee. The only sub-indexes with lower August values

included input prices, exports and imports.

Click image

for larger version

The

pace of growth in the non-manufacturing sector -- which accounts for 80% of the

economy and 90% of employment -- also quickened (+2.8PP) to 58.5%. Only input

prices and imports decelerated.

Click image

for larger version

Of

the industries we track, Wood Products and Ag & Forestry contracted in August.

Respondent comments included the following --

*

Construction: "Tariff-related cost increases are

beginning to accelerate, whether tariffs have been put into effect or not."

*

Real Estate: "Overall, business has increased.

Many factors can be attributed to this increase in demand, [including] the [federal]

budget and positive outlook on the economy."

Relevant

commodities --

* Priced higher: Corrugate; fuel; paper; transportation and trucking services;

freight.

* Priced lower: None.

* Prices mixed: Diesel and lumber.

* In short supply: Construction subcontractors; labor (construction and general);

freight; and truck drivers.

IHS Markit’s

August surveys, although still strong, were not quite as upbeat.

Manufacturing -- August PMI signals strong growth despite dipping

to nine-month low

Key

findings:

* PMI indicates strong improvement in operating conditions

* Rates of output and new order growth ease but remain solid

* Inflationary pressures soften

Services -- Service sector activity growth eases, amid weaker

new business upturn

Key

findings:

* Output and new business expand at softer rates in August

* Employment growth eases to seven-month low

* Inflationary pressures ease

Commentary by Chris Williamson, Markit’s chief business economist --

Manufacturing: "Manufacturers reported the smallest output

rise for almost a year in August, suggesting production growth could be as weak

as 0.2% in the third quarter.

"Exports

remain the key source of weakness for producers, with foreign orders barely

rising in August after two months of modest declines. The strongest growth is

being seen in consumer-facing companies, reflecting robust domestic demand, in turn

linked to the strong labor market and buoyant consumer confidence, though even

here growth has slowed.

"However,

at least some of the slowdown compared to earlier in the year reflects

production being curbed by widespread shortages of inputs, [truckers] and labor,

leading to a further build-up of backlogs of work. For producers of investment

goods such as plant and machinery, order books are backing-up at a rate not

exceeded in over ten years.

"Tariffs

and trade wars were also commonly cited as factors behind companies building

safety stocks of inputs to ensure supply or lock-in lower prices, exacerbating

supply shortages and also driving prices even higher. Looking at the survey

responses, almost two-thirds (64%) of companies reporting higher input prices

explicitly blamed tariffs as the cause of increased costs. Almost one-in-three

went on to cite tariffs as the cause of having to hike prices to customers.

Overall price pressures eased somewhat, however, which if sustained could take

some heat off consumer price inflation in coming months."

Services: “The weaker PMI numbers indicate that the third

quarter is unlikely to see the pace of economic growth match the 4.2% clip seen

in the second quarter, though it’s clear that domestic demand remains strong,

helping companies raise prices at a near-record rate.

“The

survey data so far for the third quarter signal annualized GDP growth of just

under 3.0%. However, further momentum was lost in August, and the weakest rise

in new orders for goods and services for eight months suggests growth could

wane further in September.

“Similarly,

while the survey employment readings remain roughly consistent with a non-farm

payroll gain of just under 200,000, the rate of job creation may likewise start

to slow. Backlogs of work barely rose for a second successive month in August,

indicating that existing operating capacity levels are broadly sufficient to

cope with current demand growth.

“However,

despite the signs of slower growth, companies continued to report strong

pricing power, underscoring the on-going buoyancy of domestic demand in

particular. Average prices charged for goods and services rose at a rate only

slightly below July’s nine-year survey record high.”

The foregoing comments represent the

general economic views and analysis of Delphi Advisors, and are provided solely

for the purpose of information, instruction and discourse. They do not

constitute a solicitation or recommendation regarding any investment.