Click image

for larger version

Industrial

production (IP) rose 0.4 percent in March after having increased 1.1

percent in February. For 1Q2013 as a whole, output moved up at an annual rate

of 5.0 percent, its largest gain since 1Q2012. At 99.5 percent of its 2007

average, total industrial production in March was 3.5 percent above its

year-earlier level.

Manufacturing output edged down 0.1 percent after

having risen 0.9 percent in February; the index advanced at an annual rate of

5.3 percent in 1Q. Industrial production of Wood Products decreased by 0.5

percent while Paper fell by an even greater 0.9 percent relative to February.

Click image for larger version

Click image for larger version

Click image

for larger version

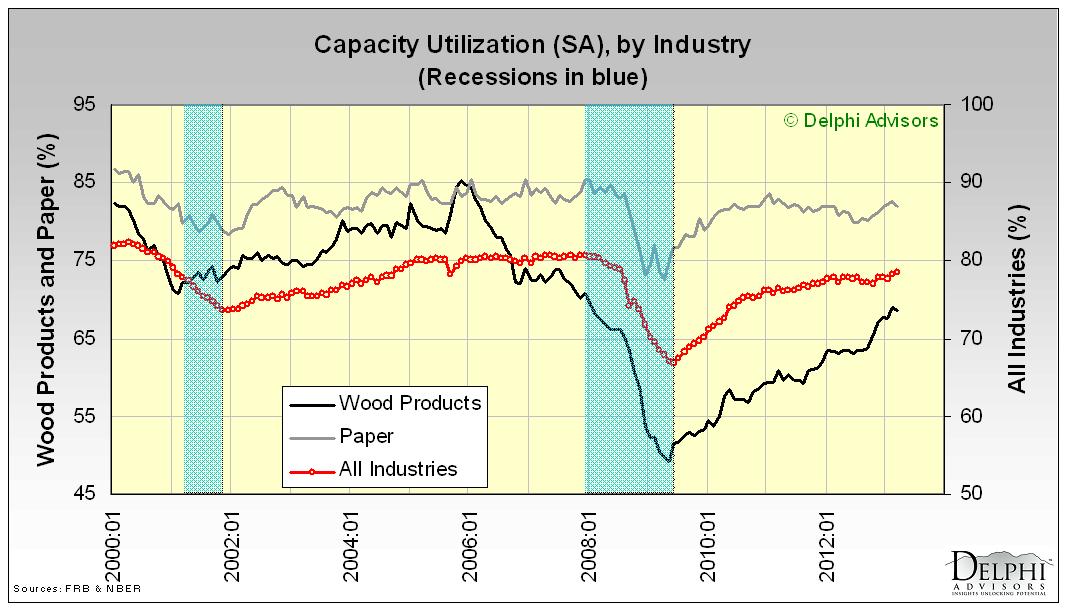

The

rate of capacity utilization for total industry moved up in March to 78.5

percent, a rate 1.2 percentage points above its level of a year earlier but 1.7

percentage points below its long-run (1972-2012) average. Capacity utilization decreased

for both Wood Products and Paper (-0.4 and -0.8 percent, respectively).

Click image

for larger version

Capacity

at the all-industries and manufacturing levels moved higher (0.1 and 0.2

percent, respectively). By contrast, both Wood Products and Paper fell by 0.1

percent.

The

Fed’s IP report was broadly consistent with the Institute

for Supply Management’s March PMI , which registered 51.3 percent, a decrease of 2.9 percentage points

from February (50 percent is the breakpoint between contraction and expansion).

March’s PMI represented the biggest miss to expectations

(of 54.0) in 13 months -- below the lowest estimate, in fact -- driven by a

collapse in new orders.

The

New York Fed’s Empire

State Manufacturing Survey is another contemporary source that is often

useful for comparison (despite the different geographic reach and time frame). The

April

2013 survey suggested that conditions for New York

To

sum up, then, one can cherry pick data to support almost any opinion of the

state of U.S.

The foregoing comments represent the

general economic views and analysis of Delphi Advisors,

and are provided solely for the purpose of information, instruction and

discourse. They do not constitute a solicitation or recommendation regarding

any investment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.